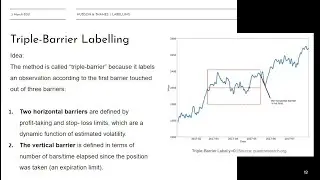

Optimal Trading Rules Detection with Triple Barrier Labeling

Join our reading group! https://hudsonthames.org/reading-group/

Labelling is a key part of any machine learning model. That is why the quantitative researcher needs to carefully chose the most optimal labelling method to solve a particular financial machine learning problem.

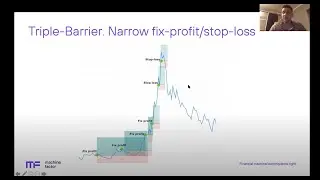

Investment management problems require domain-specific labelling techniques such as triple-barrier, trend-scanning, etc. In practice, we need to choose optimal parameters (trading rules) for labelling. For example, the triple-barrier method is a function of profit, stop-loss and maximum time in a position. Marcos Lopez de Prado suggests using Monte-Carlo simulations of a traded asset to define the most optimal trading rules.

The approach tackles the problem of overfitting parameters on a single observed path. However, the researcher needs to take into account capital restrictions and transaction costs as a function of stop-loss/fix-profit levels. With tight fix profit and stop-loss levels, the algorithm will trade more often with smaller capital allocations dedicated to each trade leading to higher transaction costs.

On the other side, by increasing maximum time in each trade, the system will trade less frequently with longer runs and bigger capital allocations. All factors described above may have a big impact on the algorithm`s risk-adjusted-performance.

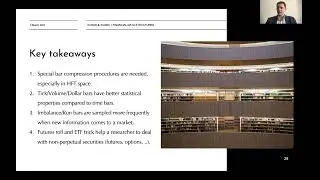

The framework suggested in this lecture shows how to choose optimal trading rules taking into account capital restrictions for meta-labelling system trading VIX futures.

Correction: MlFinLab is not open-source.