Financial Data Structures in Financial Machine Learning: Futures Roll

Join our reading group! https://hudsonthames.org/reading-group/

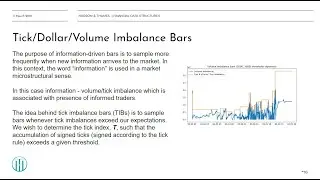

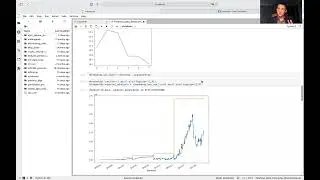

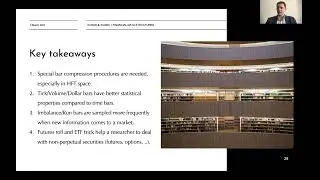

There are several caveats in backtesting futures and options strategies. Due to the non-continuous nature of this asset class, one needs to stitch them into a so-called "continuous contract."

However, naive stitching is not the correct way to deal with this problem. In our latest video, we discuss how the "Futures Roll" trick helps to solve this issue and how the mlfinlab library is used to apply the concept.