"Near Bulletproof indicator"? Constructing JPMorgans Trading Strategy [in Python] 📈VIX/S&P500

In this video we are constructing a Trading Strategy presented by JPMorgan Strategists in Python. The strategy buys the S&P500 and holds it for 6 months when the VIX (Cboe Volatility Index) rises by more than 50% of it's 1-month moving average.

Get the Notebook/Source code by becoming a Tier-2 Channel member:

/ algovibes

If you enjoy this kind of content please let me know by hitting like, leaving your thoughts and subscribing! It is a huge support for me.

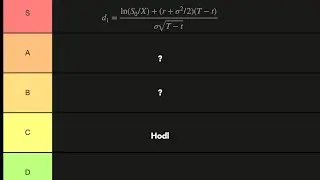

It should be noted that the last 2 mean returns are NOT YET finalized. The November signal has to be evaluated at May 26 and the January signal at July 25.

Bloomberg article:

https://www.bloomberg.com/news/articl...

How are stock returns calculated and cumultated:

• How To Calculate Stock Returns [Excel...

DISCLAIMER:

THIS VIDEO IS NOT AN INVESTMENT ADVICE AND IS FOR INFORMATIONAL AND EDUCATIONAL PURPOSES ONLY!

#Python #Trading #Strategy #VIX #S&P500

![REALTIME pull and analyze over 450 Coins with Python [SUPER SIMPLE & EFFICIENT]](https://images.mixrolikus.cc/video/SaJNtt2mFIw)

![How to pull REALTIME Cryptocurrency Prices with Python [FOR FREE] using the Binance API](https://images.mixrolikus.cc/video/P_SIZDsI3Ro)

![TRACK THE WHOLE CRYPTOMARKET WITH PYTHON [must watch]](https://images.mixrolikus.cc/video/3oRF8hgEXmU)